|

|

|

How to Avoid a Financial Model's Hidden Traps

|

|

Can your management team describe vision and strategy in terms of dollars

and cents? Can you assess whether plans are economically viable? Is your financial model aligned with your firm’s business

strategy? Will your communication of expected results withstand challenge and scrutiny?

"By failing to prepare, you are preparing to fail," noted Benjamin

Franklin, and rightfully so. Poor planning can cause shareholders and creditors to lose money, management to lose credibility,

and the entity to fail.

Developing a long-term, prospective financial model requires business insight,

focus and prioritization of competing initiatives, project organization and collaboration, effective communication, and excellent

spreadsheet design. Even then, many models fail to impress. Here are several traps and how to avoid them.

The Speed Trap

Management frequently

assumes that developing a financial model is a speedy process, requiring little more than entering a few numbers into a template.

This is seldom the case. Developing a model is a high-level, software-development initiative, heavily dependent on meaningful

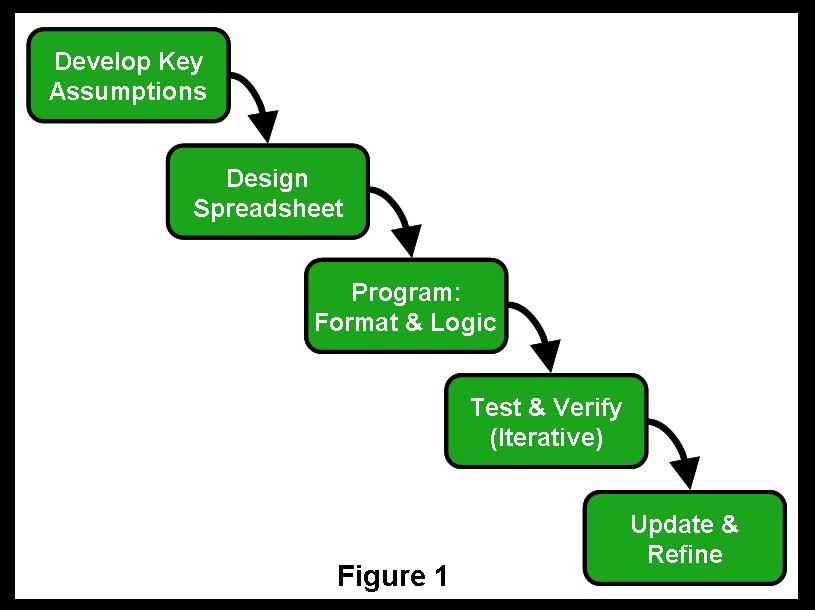

and clearly articulated business assumptions; these take time. Figure 1 shows a healthy “waterfall process” for

model development.

Your most pressing exercise is to develop key assumptions about how the business

will operate, an effort that is often shortchanged. Although essential, this information is frequently lacking, especially

in early-stage companies. Remember the mantra "garbage-in-garbage-out" and avoid wasting time designing a spreadsheet

if you cannot first articulate important strategies, opportunities or exposures, revenue and cost drivers, resource needs,

capital sources and costs, and applicable business processes.

Budget adequate time between the Program and Test/Verify processes as well.

Realize several iterations will likely be needed before management’s thinking coalesces and the model is vetted. Assume

you won’t get a second chance if you fall short the first time.

Finally, begin the project before you face an impending deadline. It is much

better to dust off and update an “evergreen” model than to hastily create one from scratch while the clock ticks.

The Boo-Boo Trap

The August 19, 2008,

edition of Business Finance magazine cites academic studies that show "...upwards of 86 percent of spreadsheets contain errors," a remarkably

high level.

Financial models by nature are complex and fraught with potential for mistakes.

Many errors are formulaic: calculations are logically incorrect, ranges of numbers are improperly defined, formulae are over-written

by predetermined results and so forth. In other cases, the relationship between financial statements is poor or nonexistent.

Common examples include cash per the balance sheet not matching the cash flow statement, or net income not tying to the cash

flow or balance sheet. At an even more basic level, eyebrows will raise when the "balance sheet...doesn’t."

Good spreadsheet development skills are helpful, but do not rely on them as

the sole control over logical and numerical accuracy. Complete a thorough self-review and have at least one “fresh set

of eyes” check key aspects of the model. Inexpensive software is available to help check for inconsistencies and mistakes.

Use these tools and techniques to avoid a boo-boo.

The Linkage Trap

Figures are meaningless

without context. Two linkage sins are common in many models. The first is a sin of omission, in which key model assumptions

are left out or are too cryptic to be of value. Second is a sin of inconsistency, in which financial model assumptions don’t

align with the business plan. Either scenario will create confusion and damage your credibility.

Instead, make sure that your packet includes a stand-alone description of

key assumptions that support the model, as well as important accounting policies and the basis of accounting used (GAAP, tax,

IFRS or others). Then perform a thorough review for consistency between the financial model and the business plan to ensure

a consistent linkage to supporting material.

The

Kool-Aid Trap

Allowing a great idea

to devolve into so much hot air is a major mistake, so don’t drink too much of your own Kool-Aid. Financial models must

be based on achievable objectives. This axiom especially applies to the top line of the income statement. Revenue is usually

the most difficult element to get right. Significant flaws can result – mistakes that can have a pervasive impact and

call into question the reliability of gross margin, variable cost, cash flow, assets and net equity figures.

Plan to spend the most research and discussion time on developing revenue

assumptions. At a minimum, management must understand and explain:

- total available market (primary market segments and specific target customers)

- competitive factors

- pricing plan

- buyer profile (who will sign your purchase order and why?)

- sales process and structure

- distribution/market channels

- other resources needed to achieve targets

Keep in mind the six P's: "prior proper planning prevents poor performance."

Your effort will pay off in an improved model and, more importantly, better decision-making and execution of top-line strategies.

The Fragment Trap

Most projections consist solely of an income or operating statement. But this is an incomplete picture

of the expected financial state of the company. It can mislead both internal and external users by masking material issues

such as cash needs and availability, ownership interests, borrowing and collateral base and so forth.

Instead of a single fragment, model a complete set of financial statements,

inclusive of the balance sheet, and statements of operations, cash flow and retained earnings. This helps ensure that parties

have the information they need to make an informed decision. And even if you distribute only a subset of that information,

the exercise of preparing it enhances management’s understanding of the business.

The Volume Trap

Determining the right

volume to present is an art, not a science. Each user digests information differently. At one end of the spectrum are highly

summarized results that provide little comfort regarding how the numbers are derived. At the other end is a data dump that

overwhelms the user with detail. Neither approach is useful.

Knowing your audience is essential. As a general rule, the model should include

detail down to a defined threshold of materiality (i.e., the key financial results, positions or relationships will not be

materially distorted if this item was missing from the model). That does not mean, however, that you will present all the

prepared information. Organize detail into meaningful groupings. Examples include: 1] summarizing monthly or weekly results

into quarterly or annual totals (columnar groupings), or 2] summarizing expenses into a total expense line (row groupings).

One variant is a traditional “layer cake” approach in which you present a summary dashboard and back it by supporting

detail. This summarized volume of information illustrates important points, while the underlying detail informs management

and inspires confidence in your presentation.

The Communication Trap

Regrettably,

many models bury key insights, important values and helpful numerical relationships amongst numerous worksheets. Forcing readers

to search through pages of data for a few nuggets of information is sure to frustrate them.

Make it easy. Include a summary page containing valuable information that

focuses on vital matters. Educated users want to see universal figures such as the predicted cash, assets, liabilities and

equity balances, as well as expected results in revenue, gross margin, net income, change in cash and EBITDA. Industry, business

environment, and the specific purpose of the model should also help you determine what additional information is useful. Examples

might include: income by business segment, headcount, key operating or liquidity ratios, earnings per employee and a host

of other possibilities.

***********************

Avoiding these perils while preparing and presenting your prospective financial

model elevates your chance for success. The outcome will be an improved model and a better prepared management team. Plus,

you will have increased your credibility. Good luck!

Click here to download a .PDF version of this document.

|

|

|

|

|

|

|

|

|

|

|

LedgerSource, LLC * 503.970.1251 * Tualatin,

OR * www.LedgerSource.com * Copyright 2009-2019

|

|

|

|